Table of Contents

- Mixed Signals from the Factory Floor

- Trump’s Vision vs. Economic Reality

- Regional Pulse: New York’s Modest Gains

- Tech Boom vs. Traditional Manufacturing

- Global Context and Challenges

- Sources

Mixed Signals from the Factory Floor

U.S. manufacturing is sending conflicting messages. While some sectors show signs of life, others continue to struggle under global pressures and shifting economic policies. This duality paints a complex picture of America’s industrial heartland in late 2025.

Trump’s Vision vs. Economic Reality

Former President Donald Trump campaigned on a bold promise: to bring factories back to American soil and revive the “Rust Belt.” But as we approach the end of 2025, the data reveals a nuanced outcome. There’s no sweeping renaissance—just pockets of growth amid persistent challenges.

While Trump-era tariffs and tax incentives did spur some reshoring, long-term trends like automation, global supply chains, and labor shortages complicate the narrative. The promise of mass factory returns remains more aspirational than actual for many traditional industries.

Regional Pulse: New York’s Modest Gains

Take New York State, for example. According to the latest Empire State Manufacturing Survey, business activity increased modestly in October 2025 . The headline index turned positive after months of contraction, suggesting a fragile rebound in one of the nation’s key industrial regions.

However, “modest” is the operative word. New orders and employment indicators remain tepid, signaling caution among manufacturers rather than exuberant expansion.

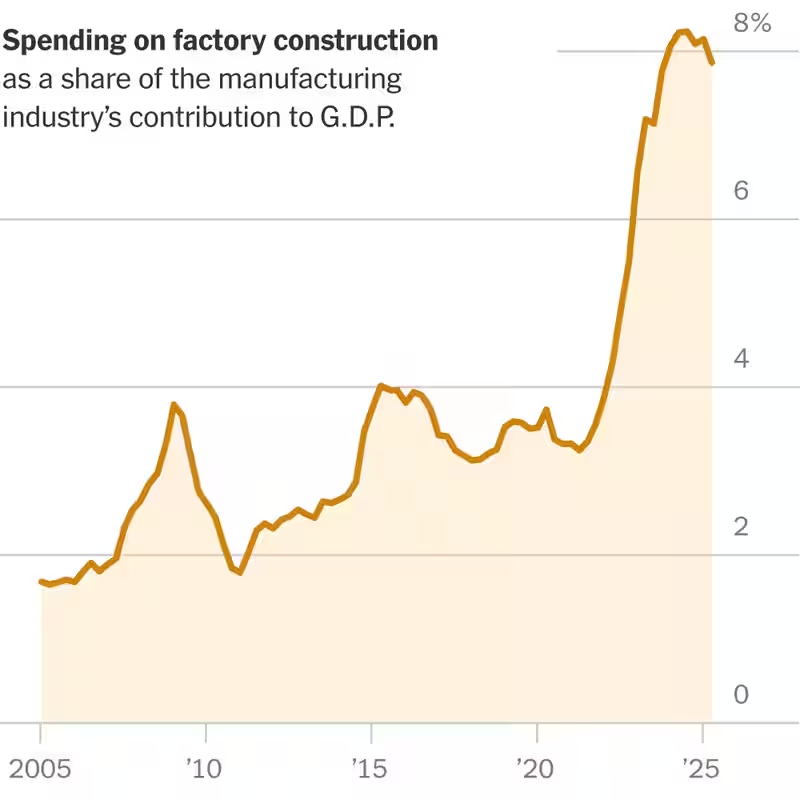

Tech Boom vs. Traditional Manufacturing

The real manufacturing momentum in 2025 isn’t coming from legacy sectors like steel or textiles—it’s driven by high-tech infrastructure. New data centers, AI-driven facilities, and semiconductor fabrication plants are arriving at a quickening pace .

This tech-fueled surge is reshaping what “manufacturing” even means. While these projects create high-paying jobs, they’re capital-intensive and employ far fewer workers than the factories of the 20th century. So while the dollar value of output may rise, the promise of mass blue-collar employment remains unfulfilled.

Global Context and Challenges

Meanwhile, global competition intensifies. China continues to execute its state-led industrial strategy through five-year plans, maintaining its edge in scale and supply chain integration . U.S. manufacturers face not just foreign rivals but also domestic headwinds: rising interest rates, skilled labor gaps, and political uncertainty ahead of the 2026 midterms.

Some critics argue that recent policies have done more harm than good. One analysis claims Trump’s return to protectionist measures “tanked the semi-successful Biden economy,” undermining stability needed for long-term industrial investment .

Sources

- The New York Times: U.S. Manufacturing’s Mixed Picture in 4 Charts

- Federal Reserve Bank of New York: Empire State Manufacturing Survey

- Utility Dive: 2025 Power Trends Report

- Financial Times: The AI Bubble and the US Economy

- Council on Foreign Relations: Economy of China

- The Nation: THE OTHER SIDE: President Trump has tanked the economy